For business decision-makers in Texas's Energy, Manufacturing, Logistics, Agriculture, and Construction sectors, a warehouse is more than a building—it's the operational core. This makes evaluating insurance for warehouse facilities a critical component of strategic financial planning. An effective risk management strategy helps protect physical assets, ensure operational continuity through disruptions, and address the unique liabilities of demanding industrial environments.

Protecting Your Warehouse from Modern Risks

A warehouse concentrates an immense amount of capital, including the structure, high-value inventory, and essential equipment. Protecting these assets requires a clear assessment of a full spectrum of risks, which extend far beyond simple fire or theft.

In Texas, these threats are often amplified by exposure to extreme weather events—a factor that increasingly drives risk management strategies for industrial operations.

Modern operational risks for Texas businesses can be categorized into key areas:

- Physical Damage: This involves direct harm to your building, machinery, and inventory from events such as hurricanes along the Gulf Coast, severe hailstorms in North Texas, or industrial fires.

- Liability Concerns: These risks arise from accidents on your property, such as a third-party contractor being injured on a loading dock or damage occurring to a client's goods while under your care.

- Operational Interruptions: A major weather event or critical equipment failure can halt operations, leading to lost revenue and significant supply chain disruption.

Understanding the core purpose of physical security safeguards is a fundamental first step. However, physical security measures alone cannot mitigate the impacts of a hurricane or widespread flooding.

The financial exposure these facilities represent is reflected in the U.S. factory and warehouse insurance market, valued at an estimated US$9.5 billion in 2024. A notable trend in this market is the increased focus on upgrading older infrastructure to meet modern standards for safety and insurability.

Disclaimer: ClimateRiskNow does not sell insurance or financial products. The information provided in this guide is for educational purposes only and should not be interpreted as financial advice or an insurance recommendation. Our goal is to equip business leaders with actionable insights to make informed decisions about operational risk management.

A resilient strategy involves two components: adequate insurance coverage and proactive risk mitigation. By analyzing your specific vulnerabilities—including the potential impacts of various natural risk examples—you can build a more defensible and insurable operation.

Understanding Your Core Insurance Coverages

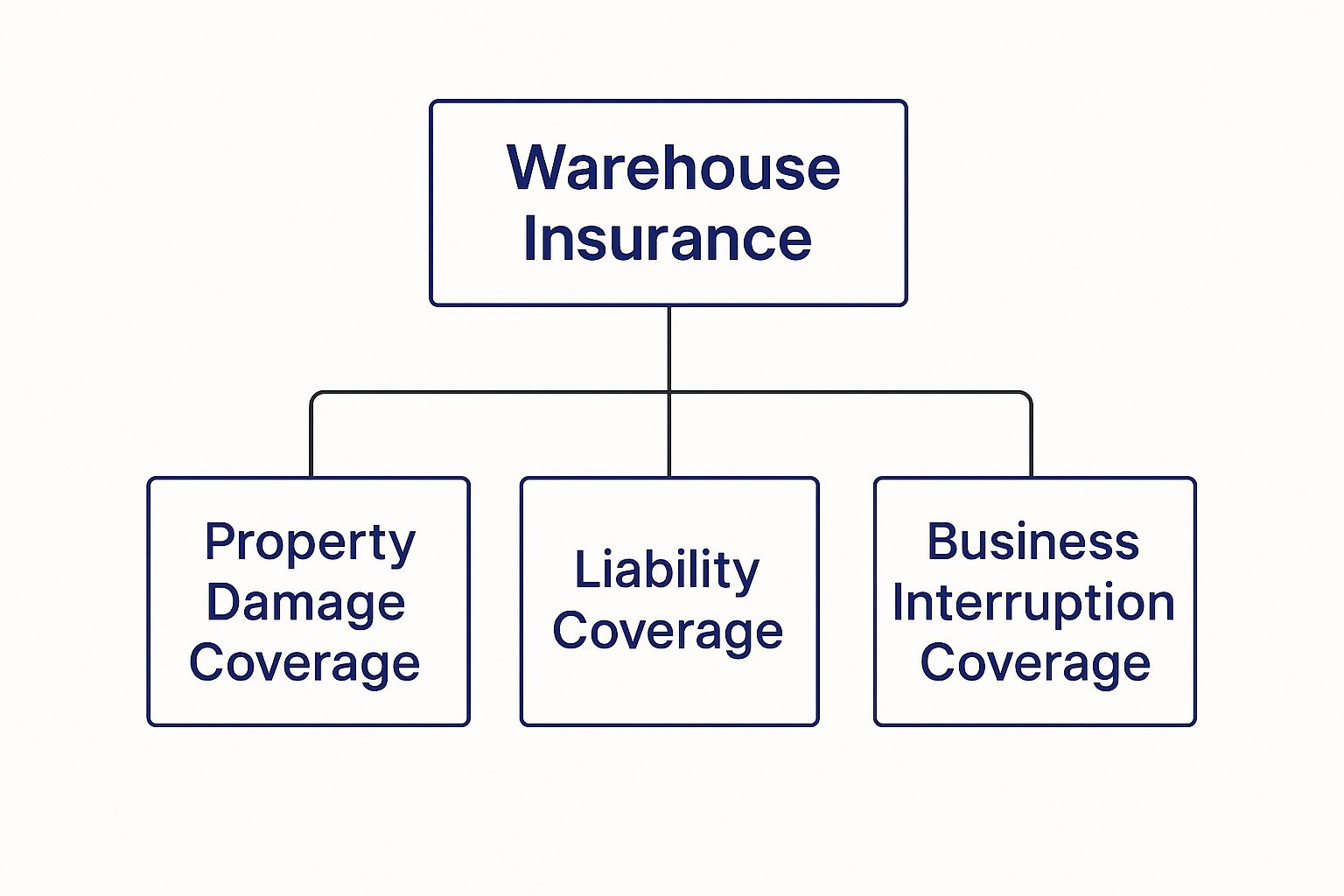

It is a common misconception to view warehouse insurance as a single policy. A more accurate approach is to consider it a specialized toolkit where each coverage type is designed to address a specific risk. For any Texas business leader, understanding these foundational components is the first step toward building an effective risk management strategy.

A solid warehouse insurance program is typically built on three pillars: Commercial Property, General Liability, and Business Interruption coverage. Each serves a distinct function, yet they work in concert to protect your assets and maintain business continuity.

A well-structured insurance portfolio should cover the building, the business's legal liabilities, and its income stream. This table breaks down the three core components with practical examples relevant to Texas industries.

Core Components of Warehouse Insurance

| Coverage Type | What It Protects | Example Scenario for a Texas Warehouse |

|---|---|---|

| Commercial Property | Your physical building, machinery, inventory, and other contents from direct damage or loss. | A severe North Texas hailstorm damages your roof and HVAC systems, leading to water intrusion that ruins stored inventory. |

| General Liability | Your legal responsibility for injuries to third parties (like clients or vendors) or damage to their property on your premises. | A delivery driver slips and falls on a wet loading dock at your Houston logistics facility, resulting in an injury claim. |

| Business Interruption | Lost income and ongoing operational expenses (like payroll) if your operations are suspended due to a covered loss. | A fire at a manufacturing plant forces a three-month shutdown. This coverage helps pay rent and salaried employees until operations resume. |

Each of these coverages acts as a critical layer of defense, shielding different aspects of your operation from financial loss.

Protecting Physical Assets With Commercial Property Insurance

Commercial Property insurance is designed to protect your physical assets—the building, essential machinery, office equipment, and inventory or goods held for clients.

For example, a major hailstorm in the Dallas-Fort Worth area can cause significant roof damage. In a coastal region like Houston, a hurricane can result in catastrophic structural failure. In these scenarios, a robust property policy provides the funds for repairs and replacements, preventing a physical disaster from becoming a complete financial loss.

It is important to note that certain high-value or specialized equipment may require a dedicated policy endorsement. You can learn more about protecting critical machinery in our guide to equipment breakdown insurance.

This breakdown illustrates how core coverages fit together, providing distinct but overlapping layers of protection for your physical assets, legal liabilities, and operational continuity.

Managing Third-Party Risks With General Liability

While property insurance covers your assets, General Liability addresses your legal responsibility when a third party is injured or their property is damaged on your premises. This is critical in a busy warehouse environment with a constant flow of vendors, clients, and truck drivers.

If a delivery driver is injured due to a hazardous condition on your loading dock and files a lawsuit, your General Liability policy would respond to the legal defense and potential settlement costs. This coverage stands between your business and the significant financial fallout from an everyday accident. For companies integrated into the e-commerce supply chain, there are often specific liability requirements; for instance, you can learn more about the rules for Amazon Seller Insurance.

Ensuring Continuity With Business Interruption Coverage

When a covered event, such as a hurricane or fire, forces a temporary shutdown, a property policy will help repair the building but will not cover the revenue lost during the downtime. This is the role of Business Interruption insurance.

This coverage is designed to replace lost income that would have been earned if the disaster had not occurred. It can also cover ongoing expenses like payroll, rent, and taxes, which is crucial for retaining key staff and meeting financial obligations until the facility is operational again. For any business in Texas, this is an essential safeguard against operational collapse following a major event.

Specialized Policies for Unique Warehouse Risks

Core property and liability policies are foundational, but they do not cover all potential exposures. Modern Texas warehouses—from sprawling petrochemical storage facilities along the Gulf Coast to agricultural hubs in the Panhandle—face a range of specialized challenges that require specific protection.

Your standard policy may protect the structure and its contents from common perils, but additional risks are tied directly to the services you provide or the specialized equipment you use. Addressing these gaps requires looking beyond basic coverages.

Covering Goods on the Move

For most Texas businesses, inventory is constantly in motion across the state's vast highway network. Inland Marine insurance is a specific policy designed to protect your goods—or your clients' goods—once they leave your warehouse and are in transit over land.

For instance, if a truck carrying high-value manufactured components from your Austin facility is involved in an accident on I-35, a standard property policy would not cover the loss. Inland Marine coverage is designed to respond to the value of the damaged or lost cargo. It is a critical coverage for logistics companies and manufacturers responsible for product delivery.

Safeguarding Critical Machinery

Modern warehouses depend on sophisticated machinery, from automated conveyor systems to large-scale refrigeration units. A sudden mechanical failure represents more than a repair bill; it can trigger a complete operational shutdown.

Equipment Breakdown coverage is tailored for this risk. It covers costs associated with the sudden and accidental failure of essential equipment. It is a vital layer of protection against the financial impact of mechanical or electrical failures, especially when those failures are triggered by stressors like extreme weather events. To learn more, you can read our guide on how to prepare for and seek insurance for natural disaster events.

The Guarantee for Stored Goods

For third-party logistics (3PL) providers and businesses that store goods for others, Warehouse Legal Liability is a non-negotiable policy. This coverage is not about protecting your own property; it is about protecting your business when you are legally responsible for damaging a client's property while it is in your "care, custody, and control."

Consider it professional liability insurance for warehouse operators. If a sprinkler system malfunction ruins a client's entire inventory, this is the policy that would respond to their claim, protecting your company's finances and reputation.

The global market for warehouse legal liability insurance was valued at approximately USD 19.14 billion in 2024 and is projected to reach USD 28.71 billion by 2030, highlighting its essential role in the logistics sector. These specialized policies are not optional add-ons; they are strategic necessities that align your insurance coverage with your real-world operational risks.

Key Factors That Drive Your Insurance Costs

The cost of warehouse insurance is determined through a detailed underwriting process where insurers assess the probability of a future claim. Understanding the variables that influence your premiums is the first step toward managing your costs effectively.

Premiums are the direct result of a comprehensive risk assessment. An insurer prices a policy based on your facility's unique risk profile, which is shaped by factors ranging from building construction to the nature of your operations.

Your Building's Physical Profile

An underwriter's initial focus is the physical structure of your warehouse. A modern, steel-frame building with a high fire-resistance rating will generally be less expensive to insure than an older, wood-frame structure. The age and condition of the roof, electrical systems, and plumbing are also significant considerations.

Location is another major driver, especially in a state as geographically diverse as Texas. A warehouse’s exposure to specific weather perils plays a massive role in premium calculations:

- Coastal Proximity: Facilities near the Gulf Coast face higher premiums due to the significant risk from hurricanes and storm surge.

- Flood Zones: Properties located in FEMA-designated flood plains, common in areas around Houston and other parts of the state, will see this reflected in their costs.

- Hail and Tornado Alleys: Warehouses in regions known for severe convective storms will naturally have higher property insurance rates.

By analyzing these location-specific threats, underwriters quantify the potential for a catastrophic weather-related loss. This data-driven approach is central to how insurers price risk, a process explored further in our article on the use of analytics for insurers.

Operational and Safety Factors

Beyond the physical structure, your day-to-day operations are scrutinized. The type of goods you store is a primary concern. Storing inert materials like textiles is considered low-risk, while handling flammable chemicals or perishable goods requiring specialized refrigeration introduces hazards that can increase costs.

Your company’s claims history is also important. A history of frequent claims, particularly for workplace accidents, signals higher risk to an insurer. Conversely, a robust safety program, thorough employee training, and a clean claims history demonstrate a commitment to risk management.

Finally, your protective safeguards can directly influence costs. A facility with state-of-the-art fire suppression systems, 24/7 monitored security, and controlled access is viewed as a better risk. These are proactive investments that lower the probability of a major loss and are often rewarded with more favorable insurance premiums.

How Proactive Risk Mitigation Improves Insurability

Viewing insurance merely as a reactive safety net is a missed opportunity. The most effective way to manage the long-term cost and availability of insurance for warehouse facilities is to mitigate risks before they materialize.

Adopting a proactive stance on risk management signals to underwriters that your operation is a well-managed risk, making you a more attractive client. This involves making strategic investments in the physical and operational resilience of your facility. For businesses in Texas facing threats like hurricane-force winds or severe thunderstorms, these upgrades can provide a significant return.

Strengthening Physical Defenses

Physical upgrades are the most direct way to harden your warehouse against potential disasters. Insurers recognize businesses that go beyond basic compliance to implement serious protective measures.

High-impact upgrades include:

- Structural Reinforcements: Fortifying your roof, walls, and loading dock doors to exceed local windstorm building codes can dramatically reduce damage from extreme weather.

- Advanced Fire Suppression: Upgrading to modern systems like Early Suppression, Fast Response (ESFR) sprinklers offers superior protection, particularly for high-stack storage configurations.

- Superior Security Systems: Integrated surveillance, controlled access, and 24/7 monitoring not only deter theft but also provide crucial documentation if an incident occurs.

Achieving Operational Excellence

While physical upgrades are critical, underwriters are equally interested in your day-to-day operational protocols. A well-managed warehouse with documented safety procedures and a culture of risk awareness is fundamentally more insurable.

Operational excellence is built on consistent, documented processes. A robust employee safety training program, for example, directly contributes to lowering workers' compensation claims. Similarly, a preventative maintenance schedule for critical equipment minimizes the likelihood of a costly breakdown and subsequent business interruption.

A well-documented business continuity plan is one of the most powerful operational tools. It demonstrates to insurers that you have a clear, actionable roadmap to recover from a major event, which can drastically reduce the financial impact of a claim.

Integrating forward-looking weather analytics into your operational planning elevates your risk management to the next level. Using advanced tools to anticipate and prepare for extreme weather demonstrates a level of sophistication that distinguishes your business. You can learn more about how to create a disaster recovery plan in our detailed guide. These proactive steps can transform your facility from a standard risk into a preferred one in the eyes of an insurer.

Looking Ahead: The Future of Warehouse Insurance

The risk landscape for warehouse operators is dynamic, continuously reshaped by powerful economic and environmental forces. Building a resilient business in Texas requires connecting today’s decisions with tomorrow’s challenges and getting ahead of trends that will define insurability and operational survival.

This means shifting from a reactive "what-if" posture to a forward-thinking "what's-next" strategy.

Two major forces are driving this change: the increasing severity of weather events in Texas and the continued expansion of global e-commerce. Both trends introduce new layers of operational complexity and liability that a standard insurance policy may not be designed to address.

The Growing Impact of Climate and Commerce

The rising frequency and intensity of extreme weather are directly impacting insurance pricing and availability. A data-driven approach to understanding your warehouse's specific vulnerability to hurricanes, floods, and freezes is no longer optional—it's essential. Insurers are now placing greater emphasis on proactive risk mitigation and rewarding businesses that can demonstrate a clear, actionable plan to withstand these threats.

Simultaneously, the e-commerce boom is placing immense pressure on warehouse operations, demanding faster turnover and more complex inventory management. This accelerated pace increases the potential for errors, accidents, and liability claims, requiring a more sophisticated risk management framework.

The financial scale of these risks is significant. The global market for factory and warehouse insurance was valued at US$35.0 billion in 2024 and is projected to climb to US$63.3 billion by 2030. This growth is driven by industrial expansion, the e-commerce boom, and the undeniable impact of climate-related events. You can explore the full research on this expanding market to understand the forces at play.

A Final Word on Resilience: Insurance serves as a critical financial backstop for recovery after a major event. However, true operational resilience—the ability to withstand and adapt to disruptions—is achieved by pairing that coverage with a smart, forward-thinking risk mitigation strategy.

Disclaimer: ClimateRiskNow does not sell insurance or financial products. The information provided throughout this guide is for educational purposes only, designed to help business decision-makers in Texas assess and prepare for operational risks.

Warehouse Insurance: Your Questions Answered

For executives managing warehouse operations in Texas, several key questions about insurance coverage often arise. Here are concise, data-driven answers.

Does My General Liability Policy Cover My Customers' Goods?

No, a standard General Liability policy does not cover property belonging to others that is in your care. This is a common and costly misconception.

General Liability is designed for third-party bodily injury and property damage claims, such as a visitor slipping and falling or your forklift damaging an adjacent property. It does not cover the inventory you hold for a client. To cover that exposure, you need Warehouse Legal Liability insurance, which is essential for any 3PL or business storing goods on behalf of others.

I'm in a High-Risk Area. How Can I Keep My Insurance Costs Down?

While you cannot change your facility's location, you can influence your risk profile. Insurers prefer to partner with businesses that demonstrate a serious commitment to risk management.

Implementing measures such as reinforcing your building to exceed local windstorm codes, installing advanced fire and security systems, and maintaining a well-documented business continuity plan can make a significant difference. Ultimately, a proven safety record with minimal claims is one of the most effective tools for managing your insurance premiums.

Is Flood Damage Included in My Standard Property Policy?

It is highly unlikely. This represents a critical coverage gap for many businesses.

Standard commercial property policies almost universally exclude damage from flooding. Given the significant flood risk across many regions of Texas, securing a separate flood insurance policy through the National Flood Insurance Program (NFIP) or the private market is a necessary step. Assuming this coverage is included in a standard policy is a gamble that can have severe financial consequences.

Don't just react to weather—get ahead of it. ClimateRiskNow provides actionable weather risk intelligence that turns complex climate data into a clear strategy for operational resilience. We help Texas-based companies understand their precise exposure to hurricanes, flooding, and other severe threats. Request your comprehensive risk assessment today.